TDS under section 194-IA

Introduction: What is TDS Under Section 194-IA?

When you purchase an immovable property in India valued at ₹50 Lakhs or more, you — as the Buyer — are legally obligated to deduct Tax Deducted at Source (TDS) at the rate of 1% of the total transaction value. This obligation is governed by Section 194-IA of the Income Tax Act, 1961.

This rule applies uniformly to all types of property transactions — whether it is a new purchase directly from a builder under a Construction Linked Plan (CLP), or a secondary/resale transaction between two individuals. The key principle is simple:

"The Buyer must deduct 1% TDS on the total deal value and deposit it to the Income Tax Department on the Seller's PAN — irrespective of whether the builder payment is pending or not."

Need help with property legal services or TDS filing? Visit BazaarX Legal & Registration Services for expert assistance.

Applicability of Section 194-IA

Section 194-IA applies to the following scenarios:

- Purchase of residential or commercial immovable property valued ₹50 Lakhs or more

- Both new builder purchases (CLP) and resale/secondary market transactions

- NRI property buyers (separate rules may apply under Sections 195 and FEMA)

- All buyers — individuals, companies, HUFs, partnerships, trusts

- Transactions in both urban and rural areas

📌 Note: Agricultural land is EXCLUDED from the purview of Section 194-IA and does not attract TDS under this provision.

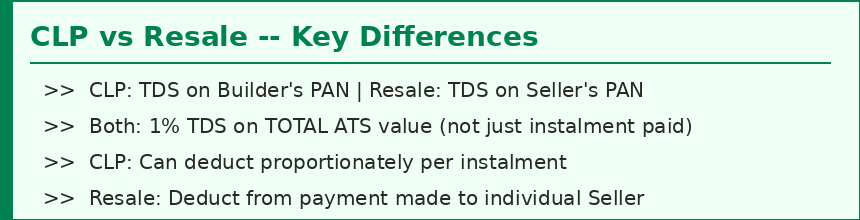

TDS on CLP (Construction Linked Plan) Transactions

In a Construction Linked Plan, the buyer makes payments to the developer in instalments, linked to various stages of construction — such as foundation, slab, plinth, possession etc.

How TDS is Calculated in CLP:

Under CLP, the total Agreement to Sell (ATS) value is the agreed purchase price, regardless of the payment schedule. The TDS obligation is:

- TDS is deducted at 1% of the total ATS value, NOT just the instalment paid

- TDS can be deducted proportionately on each instalment, as long as the cumulative TDS equals 1% of the total ATS

- It must be deposited WITHIN 30 days from the end of the month in which TDS was deducted

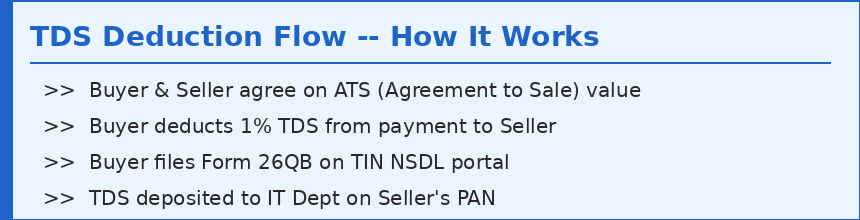

- It is credited against the Seller's (Builder's) PAN

Common Confusion Clarified:

Many buyers incorrectly assume that TDS is only applicable on instalments actually paid. This is INCORRECT. The Income Tax Department requires TDS based on the total agreed deal value. Even if 40% of the payment is pending, TDS must reflect 1% of the FULL ATS amount.

📌 Note: Example: If ATS value is ₹1 Crore, total TDS to be deposited is ₹1 Lakh (1%) — regardless of payment timeline to builder.

Explore property financial planning tools at BazaarX Finance Services.

TDS on Resale (Secondary Market) Transactions

In a resale transaction, property is purchased from an existing owner (Seller) rather than directly from a builder. The same 1% TDS rule applies here as well.

Key Points for Resale Buyers:

- TDS must be deducted from the payment made to the Seller

- It is deposited on the PAN of the Seller (not the original builder or developer)

- Total TDS = 1% of the full transaction value, as per the registered Sale Deed / ATS

- Buyer must issue Form 16B (TDS Certificate) to the Seller within 15 days of filing Form 26QB

- The Seller can claim this TDS as credit against their tax liability while filing ITR

Important: TDS on Seller's PAN vs Builder's PAN

A critical point often misunderstood in resale transactions is which PAN to use for TDS:

- In CLP (builder purchase): TDS is deposited on the BUILDER's / DEVELOPER's PAN

- In Resale: TDS is deposited on the CURRENT SELLER's PAN

- NEVER deposit TDS on the original builder's PAN in a resale transaction

📌 Note: Depositing TDS on the wrong PAN is a compliance error and may attract penalties. Always verify the Seller's PAN before filing Form 26QB.

Step-by-Step Process for TDS Deduction & Deposit

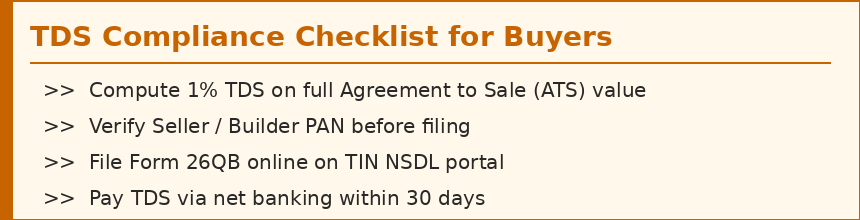

Step 1 — Compute the TDS Amount

Calculate 1% of the total Agreement to Sale (ATS) value or stamp duty value (whichever is higher). This is the amount to be deposited to IT.

Step 2 — Deduct from Seller Payment

While making any payment to the Seller, retain 1% as TDS. You may deduct this upfront in one payment or proportionately across multiple transactions.

Step 3 — File Form 26QB

Log in to the TIN NSDL portal (https://tin.tin.nsdl.com) and fill Form 26QB — the challan-cum-statement for TDS on immovable property. Details required include:

- Buyer's and Seller's PAN, name, and address

- Property address and type

- Total transaction value and TDS amount

- Date of payment / agreement

Step 4 — Pay the TDS

After filling Form 26QB, pay the TDS amount via net banking or at an authorised bank branch. The acknowledgement number must be saved.

Step 5 — Issue Form 16B to Seller

Download Form 16B (TDS Certificate) from the TRACES portal and provide it to the Seller within 15 days from the due date of filing Form 26QB.

Need help filing Form 26QB? BazaarX Accounting & Compliance Services can guide you through the entire process.

Quick Reference: Key Facts at a Glance

|

Parameter |

Details |

Remarks |

|

TDS Rate |

1% |

Of total deal value |

|

Applicable Section |

194-IA |

Income Tax Act |

|

Who Deducts |

Buyer |

Mandatory duty |

|

Threshold |

₹50 Lakhs+ |

Property value |

|

Form to File |

Form 26QB |

Online on TIN portal |

|

TDS Certificate |

Form 16B |

Issued by buyer |

|

Deposit Deadline |

30 days |

From end of deduction month |

|

Seller PAN |

Mandatory |

TDS credited on seller PAN |

Penalties for Non-Compliance

Failing to deduct or deposit TDS can lead to serious legal and financial consequences for the Buyer:

- Interest @ 1% per month for failure to deduct TDS

- Interest @ 1.5% per month for failure to deposit TDS after deduction

- Penalty under Section 271C — equal to TDS amount not deducted

- Prosecution under Section 276B — imprisonment from 3 months to 7 years in severe cases

- Disallowance of property purchase expense in case of business buyers

📌 Note: Non-deduction of TDS does NOT cancel the sale, but it creates a tax liability for the Buyer that must be settled separately.

Frequently Asked Questions (FAQs)

Q1. What if the ATS value is below ₹50 Lakhs?

Section 194-IA does not apply if the total property value is below ₹50 Lakhs. No TDS needs to be deducted in such cases.

Q2. Is TDS required on stamp duty and registration charges?

No. TDS is calculated only on the transaction value as per the sale agreement (ATS), excluding stamp duty and registration fees.

Q3. What if the property has multiple sellers?

If the property has joint sellers, TDS must be deposited separately on each Seller's PAN, in proportion to their ownership share.

Q4. What if the Seller is an NRI?

If the Seller is a Non-Resident Indian (NRI), TDS rates are higher and governed by Section 195, not 194-IA. In such cases, consult a tax expert or CA before proceeding.

Q5. Can the Seller apply for lower/nil TDS deduction?

Yes. The Seller can apply to the Assessing Officer for a lower/nil deduction certificate under Section 197. If granted, the Buyer must deduct TDS at the reduced rate.

Have more questions? Connect with BazaarX experts at www.bazaarx.co/contact.

How BazaarX Can Help You

BazaarX is a one-stop platform for all your real estate financial, legal, and compliance needs. Here is how we help buyers and sellers navigate TDS under 194-IA:

- Expert CA/CS professionals to file Form 26QB accurately and on time

- End-to-end legal support for property registration and documentation

- Digital tools to compute TDS liability on CLP and resale deals

- Verification of Seller/Builder PAN and transaction details

- TDS certificate (Form 16B) generation and delivery

🏠 Explore our Real Estate Services | Finance & Tax Services | Legal & Registration

📚 Read more guides at our BazaarX Blogs and BazaarX Academy.

Conclusion

Section 194-IA is a mandatory compliance requirement for every property buyer in India, whether the transaction is a fresh CLP purchase from a builder or a resale deal in the secondary market. The golden rule is:

Deduct 1% TDS on the Total ATS Value and Deposit it on the Seller's PAN — Always and Without Exception.

Ignoring this requirement is not just a financial risk — it is a legal liability. Stay compliant, stay protected.

BazaarX — Empowering Your Property Journey

🌐 Visit us: www.bazaarx.co | Find Property | Become a Partner